Flexible Spending Accounts 🧾

Here's how Flexible Spending Accounts (FSAs) can save you $100-$2,000 on taxes every single year.

Many employers offer Flexible Spending Accounts (FSAs) that can help you save money on taxes, but not everyone understands how they generally work.

Health FSA

Health FSAs are employer-established plans that allow you to contribute money pre-tax to pay for certain medical or dental expenses. Employers have considerable flexibility in how they design these plans, so be sure to read the specific details of yours.

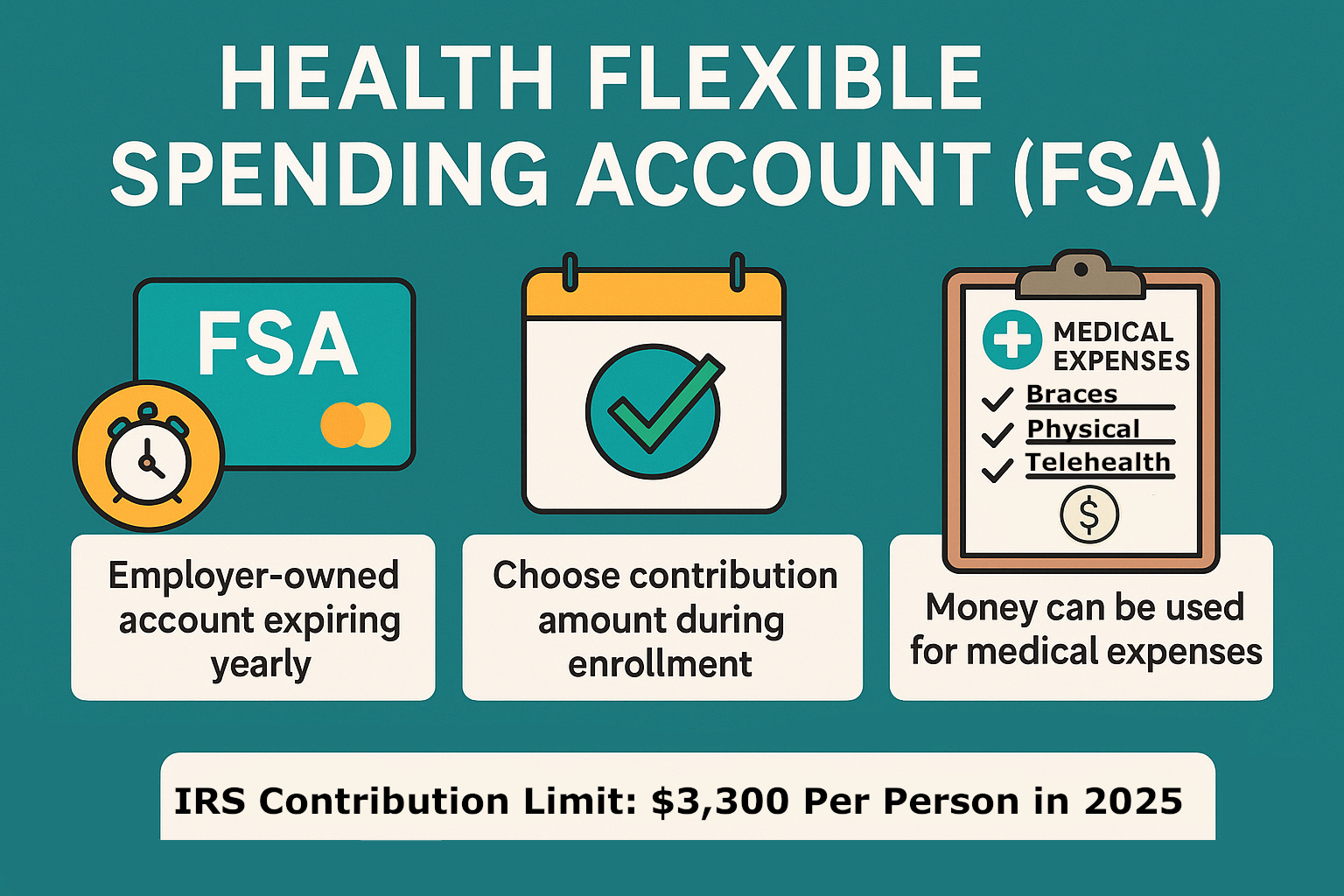

Think of a Health FSA like a gift card provided by your employer, but the money expires within a year if you don’t use it.

You can enroll in a Health FSA, if your employer offers it, only during the enrollment period. At that time, you designate how much you want to contribute to the FSA.

For 2025, the IRS maximum limit is $3,300 per person, but check your specific plan for the allowed contribution. If you’re married and your spouse also has an FSA, you can contribute up to $6,600 total, but you can’t “double-dip” by reimbursing the same expenses from both accounts.

At the beginning of the year, you decide how much you want to contribute.

Then, throughout the year, your employer will deduct amounts every pay period.

For example, if you want to put in $1,000, the employer will split that $1,000 equally over the pay periods and withdraw it every x weeks. However, this $1,000 is available right away for you to spend.

What does the health FSA reimburse?

You can use the health FSA to cover:

Braces and retainers

Medical, dental or vision office visits

Prescription sunglasses, contact lenses and solutions

Telehealth/remote care

Physical exams and therapy

Supplements (with a Letter of Medical Necessity)

Certain health related travel costs

Newborn care, nasal sprays, pain relievers, and nose strips

Here’s a full list of eligible expenses, but you can also refer to the IRS Publication 502 for more details.

Note: You cannot use an FSA for health insurance premiums, long-term care coverage, or expenses covered by another health plan.

Quick summary visual:

Example

Because the Health FSA expires if it’s not used throughout the year, you should only contribute the amount you reasonably expect to spend.

For example, say you are a high earner with a 37% marginal tax rate and a 6% state rate. Your daughter wants to get braces this year, so you know you’ll reasonably spend around $2,000.

You decide to enroll and contribute $2,000 to a Health FSA. This saves you about $860 on taxes for something you would’ve spent money on anyway.

If you don’t have a need to spend on something expensive like braces, just lower the amount to what you think you’ll spend based on prior years, like annual physicals, lenses, or prescriptions.

Use it or lose it

Like I mentioned earlier, your Health FSA balance will expire if you don’t use it. However, some employers might offer the following (check your plan to be sure):

A rollover option into the next year (up to $660 max, per IRS limit)

A grace period of up to 2.5 months to spend unused funds

Also, if your money is about to expire, you can stock up on items you’d use anyway (e.g. contact solution).

Quick plug

If you want to receive in-depth subscriber only tax planning posts, access a community, comment, and view archives, consider supporting my publication by becoming a paid subscriber.

Leaving your job

If you leave your job and haven’t spent the FSA money, you will forfeit the balance. If you get laid off, you will also forfeit the balance (unless you can quickly run to the store before getting laid off).

But the rules also work in your favor: you can spend the full FSA amount (even if you haven’t contributed it all via payroll) and don’t have to pay it back if you leave your job.

HSA vs Health FSA

You cannot have both a Health FSA and a Health Savings Account (HSA), unless your plan offers a Limited Purpose FSA (LPFSA), in which case you can. LPFSA follows similar rules as above, but check your plan specifics.

However, an HSA is better because the amounts don’t expire. But if you don’t qualify for an HSA due to not having a high-deductible health plan, then an FSA can be useful.

Dependent Care FSA

Some employers also offer a Dependent Care FSA (DCFSA).

It’s a similar deal to the Health FSA but is used for dependent care services such as summer camps, after-school programs, or daycare for a dependent under the age of 13.

You get to save money on taxes by contributing to something you would’ve spent money on anyway.

Unlike the Health FSA, where an employer funds it all at once and then withdraws from your paycheck equally over the year, you contribute to a Dependent Care FSA as the money is withdrawn every pay period.

The contribution limit for 2025 is $5,000, or $2,500 per year if you are married filing separately. If you and your spouse are both eligible to contribute to a DCFSA, you cannot exceed the $5,000 limit combined (i.e. it is shared between both spouses).

However, if you are a highly compensated employee (earning $160k/year or more), a lower contribution limit might apply (check with your plan)

Summary

Not a lot of people utilize these FSAs, but they can be a great way to save at least a few hundred dollars in taxes every year.

If you have any questions, please reach out.

Talk next Saturday.

-MC, CPA