Invest or Pay Down Debt?

Here's how to make the right choice on debt vs investing...

I often receive messages like “Should I invest or pay off my debt?”

It’s literally impossible to answer such questions without knowing interest rates, liquidity, your stage in life, age, net worth, loan product, and risk appetite, but there is a general framework we can follow.

Debt vs Investing

You’ve probably heard something along the lines of “Just compare the interest rate on your debt with investment returns, and put the money toward the option with the highest percentage!”

In theory, that absolutely makes sense for many clear-cut cases, but we also have to examine other non-financial and risk-adjusted factors too.

Clear cut cases

Jonathan is 25 and makes $60,000/year. He has an employer 401(k) match of 3% that he isn’t using, and a credit card debt of $10,000 at a 20% APR. After expenses, he has $500/month to put toward investments or credit card debt. What should he do?

The obvious answer is to:

Invest 3% in a 401(k) to receive the 3% match. This will be ~$150/month invested.

Put the rest ($350 if he chooses the Roth option) toward paying off his credit cards fast.

So, investing up to the match first and paying off your credit cards quickly is an easy choice.

The second clear cut case: I believe any debt below 4% shouldn’t be paid off early. With inflation and opportunity cost, I just don’t think it’s worth it.

More trickier situations (4-8% range)

Let’s now say Jonathan is making $60,000/year. He has an employer 401(k) match of 3% that he is taking. He also has a 5% student loan of $10,000. After expenses, he has $500/month to put toward investments or student loans. What should he do?

What does the research say?

Researchers conducted a set of experiments in “The Opportunity Cost of Debt Aversion” asking participants to manage accounts with different interest rates and balances. Each person was also randomly assigned a specific amount of debt. The goal was to see how debt impacts financial decision-making, specifically whether people would choose to pay off debt or invest in accounts with higher returns.

The results were clear – many people didn’t like being in debt. In fact, 1/3 of participants focused heavily on paying it down, regardless of better investment options being available.

So even if the investment return is guaranteed and financially superior, many people would still prefer to pay off a loan.

Clearly, the psychological impacts are profound, and debt aversion is real. Some people view it as a completely negative thing, while others don’t.

This is exactly why the 4–8% interest rate range is especially tricky.

p.s. want to support my work? Become a paid subscriber for an exclusive access:

What should Jonathan do?

As the research indicated, for some people this is an emotional decision, not a financial one. They just want to get out of debt, even if it’s not harming them financially.

The way I see it is:

Jonathan is young, his risk tolerance is high, and he’s investing for the long term. He can weather any downturns in the market and will likely earn the average 8% returns over time. With his 5% loan, it probably doesn’t make sense to pay it off early.

Of course, future investment returns aren’t guaranteed, especially in the short term. In contrast, the “return” you get by paying off your loan early is guaranteed (unless you refinance to a lower rate, which can complicate the calculation).

What if his student loan rate were 7%?

In that case, you really can’t go wrong. If you’re unsure, splitting it 50/50 is a decent choice.

There are also some important qualitative factors that we need to consider

Liquidity

If you need the money later, beyond your emergency fund or savings, it’s hard to get it back if you’ve already used it to pay off something like student loans early. Of course, this also depends on your overall net worth and access to other liquid options.

Discipline

It takes discipline to continue investing when you have cash available. This is why, depending on your personality, paying off debt early might be a fine choice.

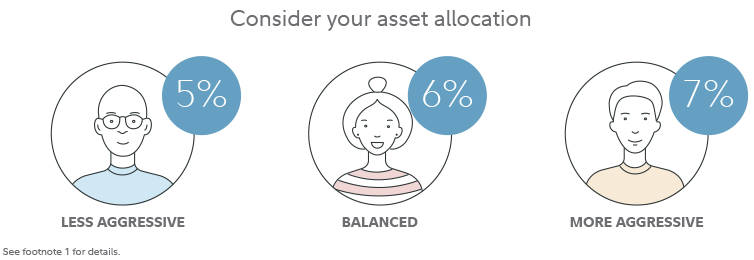

Fidelity’s input

Fidelity looked at asset allocations (less aggressive (20% stocks), balanced (50% stocks), or aggressive (100% stocks)), applied a 70% confidence level to expected market returns, and based on that analysis, they recommended paying off any debt higher than the following interest rates, depending on your allocation:

I think most people fall into the balanced or more aggressive range, and these interest rate thresholds are relatively reasonable.

Final thoughts

The most important factor is that you’re doing something to improve your net worth either way.

Pay off your loan early, assuming it’s not a part of the clear cut choices. Don’t pay off your loan early, but invest instead. Whatever path you choose, just keep focusing on improving your financial situation and putting more of your money to work.

p.s. want to support my work? Become a paid subscribe to receive an exclusive access: