Roth IRA Emergency Location 💰

How Roth IRA can be used as an emergency fund location (and save you on taxes)

Did you know that you could temporarily hold your emergency funds in a Roth IRA?

It might sound counterintuitive, but it makes a lot of sense in some specific scenarios.

Case example

Josh has a $10,000 emergency fund in a HYSA earning 4%.

This emergency fund generates $400/year in interest, which is subject to tax of, say, $120/year.

Josh is also contributing to a 401(k), but not enough to max out both the 401(k) and Roth IRA.

Josh contributed $7,000 in 2024 (the maximum limit) to a Roth IRA from his emergency fund.

The overall amount Josh has for emergencies is still $10,000, but it’s now split between $7,000 in a Roth IRA and $3,000 in his HYSA.

Importantly, the $7,000 amount is NOT invested in index funds like the S&P 500 or Total Market US. It’s in a conservative money market fund earning a similar 4.19% yield, so there is no market risk.

On June 25, 2025, Josh signed a new job offer with an amazing $15,000 after-tax sign-on bonus.

Replenishing

Josh now wants to put that $15,000 to use. He puts an additional $7,000 into a Roth IRA for 2025.

He then also replenishes the $7,000 (that he put in a Roth IRA in 2024) in his HYSA emergency fund.

The Roth IRA account ($7,000 from 2024 and $7,000 from 2025) can now both be invested.

What’s the point?

Since Josh didn’t have an emergency between 2024 and 2025, he’s preserved tax-advantaged space he could later invest within.

If he had held the money in a HYSA and never contributed to a Roth IRA, he’d lose the opportunity to fund that Roth space for the year (you can’t “catch up” after the deadline).

With this strategy, Josh was able to contribute to both 2024 and 2025 to his Roth IRA.

If he hadn’t shifted some of the emergency funds to the Roth, even with his bonus, he would only be able to do it for 2025, as the deadline for 2024 had passed.

In addition, out of the initial $400 in interest per year, $280 of it will now be inside a Roth IRA, saving ~$85/year in taxes.

What if Josh needed that money for an emergency?

Remember that Josh shifted $7,000/$10,000 from his HYSA to the Roth IRA.

BUT Roth IRA contributions can always be withdrawn tax- and penalty-free at any time.

This means that if Josh needed $10,000 for an emergency, he could’ve just pulled $7,000 from the Roth and $3,000 from the HYSA.

In this case, you lose nothing.

What this strategy accomplishes is just the location of the funds, not the amount.

Again, the Roth shouldn’t be invested in any equity funds, as they could drop at the time you need a withdrawal.

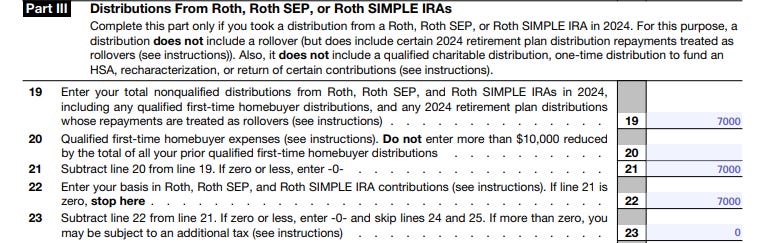

During tax time, withdrawals from a Roth IRA need to be reported on Form 8606:

The example above uses a $7,000 contribution and $7,000 withdrawal.

Other use cases

1. Building emergency

In our example, we started with someone who already has an emergency fund.

But you can also use a Roth IRA to build your emergency fund. In that case, simply contribute the emergency funds to the Roth and put them in stable funds.

Once your emergency fund is built, and you want to invest, simply invest the money inside the Roth IRA and “transfer” the same amount to the HYSA.

2. Saving for large future expenses

Say you are saving for a down payment. It could take you a few years to save enough for a 3.5% down payment.

If you use a Roth IRA and end up needing less than projected, you could just invest that money instead.

Summary

Is the juice worth the squeeze?

For some, it might, especially when saving for large future expenses.

But for others, it may not.

If you do decide on something like this, you must have the discipline and commitment to keep the emergency fund portion of a Roth IRA separate from the retirement portion.

Also, withdrawals from a Roth IRA might take a few days to complete.

Want to support my writing and receive premium content? Consider becoming a paid subscriber.

See you next Saturday.

MC, CPA